California House Hunters Are Balking at High Home Prices – Just Like Their Fellow Americans

In the sun-drenched suburbs of Los Angeles, a couple stands outside a charming two-bedroom home with a white picket fence. Their hopeful expressions quickly shift to dismay as they check the price: a staggering $1.2 million. This scene has become increasingly common as California’s housing market experiences a severe rejection from buyers, mirroring trends across the United States, yet with a significant twist: the ‘no-go’ price point here dwarfs the national average.

A Fractured Market Landscape

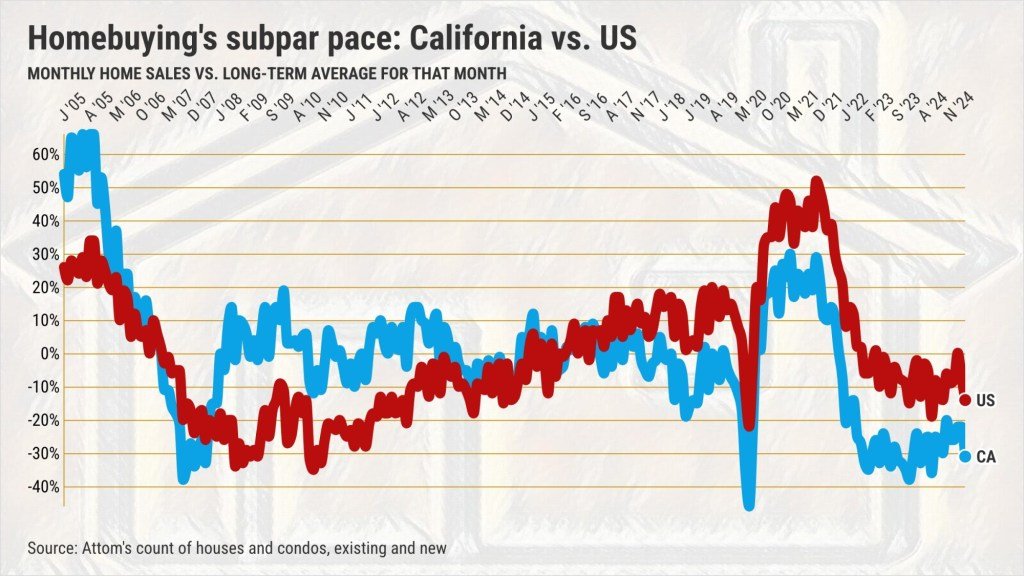

Forget the chatter around a buyer’s market versus a seller’s market; neither appears to be thriving in California, leaving many to dub it a “nobody’s market.” The latest figures from Attom’s April sales report offer a potent reminder of just how harsh the reality has become. This report indicates that April’s home sales were the fourth-worst in California over the past two decades, contributing to a nationwide sentiment of unrest in the housing sector.

While California sales rose by 2% year-on-year, the national average fell by 8%. Yet, California’s numbers tell a different story: they’re still 23% below the historical pace for April, marking the 35th straight month that home sales have lagged behind the expected norm. Nationally, sales have dipped just 10% below par, pointing towards a fragile equilibrium in the broader real estate market.

The Price is High

At the heart of the issue lies the relentless rise in housing prices. In April, California’s median home price reached $750,000—a slight increase of only 1% compared to the previous year. For context, this figure matches the all-time high set just a year prior. In contrast, the national median price climbed to $364,000, just $1,000 shy of breaking its own record.

- California’s median home price: $750,000

- National median home price: $364,000

- Sales velocity: 23% below state historical average for April

- California’s pricing increase over six years: 50%

- National increase over the same period: 58%

As such, the market has thinned to a demographic of wealthier buyers who can afford to gamble on overvalued properties. “Families looking to buy a home in California are increasingly priced out of the market,” notes Dr. Anna Rodriguez, a real estate economist at Stanford University. “This is not merely a local issue; it’s reflective of the growing-income disparity in our society.”

Mortgage Rates and Buyer Burden

The financial landscape has further compounded these challenges. The average 30-year fixed mortgage rate stood at 6.7% for the three months ending in April, compared to 6.9% the previous year. This dramatic shift marks an alarming increase from the 4.3% rates observed six years ago, before the pandemic triggered widespread market upheaval.

For a hypothetical buyer seeking to purchase a median-priced California home, this means a staggering monthly payment of approximately $3,888—assuming a 20% down payment. This figure is up a shocking 97% over six years. To draw a further comparison, the typical American buyer’s monthly payment is now around $1,887; similarly, it has risen by 108% during the same period. “With mortgage rates where they are, only the affluent can enter these discussions,” says Mark Ellis, a financial consultant specializing in real estate investments.

The Affordability Gap

The crux of the issue remains the stark disparity between wage growth and escalating living costs. In the past six years, average weekly wages increased by 25% in California and 29% nationally. Yet, housing prices have surged far beyond these earnings. “In real terms, what you are seeing is not just an affordability crisis but rather a systemic failure to provide adequate housing for everyday Americans,” asserts Dr. Margaret Nguyen, a sociologist at UCLA who has been studying Californian housing trends.

Some analysts argue that a decrease in mortgage rates could bring temporary relief; however, even with a drop back to the 4.3% rate from April 2019, buyers would still grapple with exorbitant price tags that reflect an overall increase of near 50% in California. The notion that an increase in housing supply would alleviate buyer woes has proven misguided, as options abound yet buyers continue to shun overpriced listings.

Demand for Discounts

Sellers, both individual homeowners and large developers, are stuck in a challenging limbo. Without price adjustments, their properties will likely linger unsold. Regardless of the terminology—be it concessions, adjustments, or incentives—the message remains clear: it’s time for housing prices to meet the realities of a lackluster market. As financial analysts commonly illustrate, when retailers face inventory build-up due to overpriced goods, they don’t hesitate to mark down prices.

This bleak scenario suggests a pressing need for a recalibration of the housing market, especially in California. “It’s about time that the homes on the market reflect their true value, rather than arbitrary price tags based on speculation,” remarks real estate agent Lisa Chen, who has witnessed the market heat up and cool off over the years. “Only then can we hope to see buyers returning to the table.”

As the California housing market navigates this stormy sea of inflated prices and skyrocketing costs, the questions linger: Will homes ever be affordable again? Or will this “nobody’s market” continue to force prospective buyers into a retreat, leaving behind empty houses and shattered dreams under the shining California sun?