California’s Home Sales Decline: A Deepening Crisis in the Real Estate Market

As dusk settled over a quiet cul-de-sac in Sacramento, the “For Sale” sign swayed gently in the warm breeze, its bright colors a stark contrast to the somber reality of a stagnant housing market. Once vibrant neighborhoods now echo with uncertainty as California’s home sales have plummeted, recording the largest decline in a year this past May. The clamor of eager buyers has quieted, leaving only whispers of worry among prospective homeowners.

Declining Sales Amid Rising Prices

According to data from Attom, the state recorded 28,557 closed sales of houses and condos in May, marking a 7% decrease from the previous year. “California’s market is experiencing a pronounced buying slump, exacerbated by elevated prices and mortgage rates,” explains Dr. Sarah Whitaker, a real estate economist at the University of California. “The economic uncertainty is palpable, and many buyers simply do not feel confident moving forward.”

The current sales figures are alarming: down 29% from the average of 40,261 sales in May since 2005. May 2025 stands out as merely the second-slowest month for home sales in over two decades. This stagnation reveals a deeper malaise within California’s real estate landscape, as the total number of homes sold over the past year reached just 324,326—26% below the average pace over the last twenty years.

Price Pressures Persist

While sales have steadily declined, those who are buying are facing colossal price tags. The state’s median selling price of $750,000 in May ties the peak established back in June 2024. Prices are not rising, however; the median price has only increased by a scant 0.1% over the past year. “The current performance of home prices is the worst we have seen in 24 months,” notes Jonathan Fleischer, a senior analyst at Market Insights. “Potential buyers are increasingly sensitive to pricing trends, and many are waiting to see if the market will adjust.”

- The median home price has stagnated at $750,000.

- May recorded the worst performance for home prices in two years.

- Home sales are at their lowest level in 21 years for May.

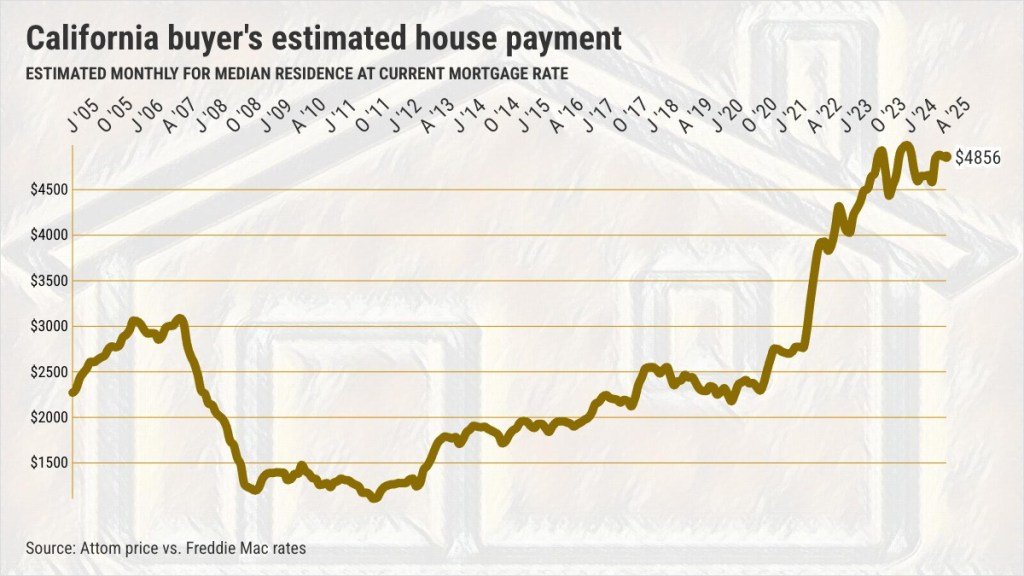

Payment Pain: The Financial Squeeze

For the majority of homebuyers, reality bites hard, with high prices paired with soaring mortgage rates. In the three months leading up to May, borrowers secured a 30-year fixed mortgage at an average rate of 6.8%, slightly lower than the 7.1% recorded in May 2024, yet significantly higher than the 4.1% rates prior to the pandemic. “The sustained elevated rates mean that many would-be buyers simply cannot afford to purchase a home,” asserts Dr. Whitaker.

The implications are stark. A typical buyer in May faced an estimated monthly payment of $4,856, making it the ninth-highest on record. This translates to a down payment of $150,000 for the median-priced home. Even more troubling, this buyer’s burden is now double what it was six years ago. “The affordability crisis is real,” laments Annika Roberts, a financial planner specializing in real estate costs. “Young families and first-time buyers are especially hit hard, as they struggle to save enough for substantial down payments while navigating rising expenses.”

The Bigger Picture: Economic Indicators

The current stagnation in the housing market reflects broader economic pressures. Inflation remains a formidable challenge, exacerbating financial strains for many families. A recent survey conducted by the California Economic Review indicated that a staggering 67% of respondents believe now is not the ideal time to invest in real estate. “Consumer confidence has tanked, with many uncertain about their job security and future financial stability,” notes Marcus Cheng, director of the survey.

Looking Ahead: Cautious Optimism?

Despite the challenging landscape, some analysts theorize a potential turn in the tides. “Given the cyclical nature of real estate, we could see a rebound, especially if mortgage rates begin to retreat later this year,” posits Marcus Cheng. “However, any upcoming changes in the Federal Reserve’s interest rates will play a crucial role.”

As various communities across California grapple with the implications of slumping sales and stubbornly high prices, potential homebuyers are left at a crossroads. For many, the dream of homeownership seems increasingly elusive. Yet amid the uncertainty, stories of resilience persist. Local organizations are stepping in to help first-time buyers navigate financial barriers, fostering a glimmer of hope amid a challenging landscape.

As the sun set behind the Sacramento houses, the “For Sale” signs seemed to sag a little more, overshadowed by the weight of financial insecurity. But just as every dusk is followed by dawn, the people of California await the changes that may reshape their housing market, hoping for accessibility, affordability, and ultimately, the opportunity to call a house a home.