Why So Few Home Sales in Los Angeles and Orange Counties?

In the shadow of palm trees and high-rises, the once-thrumming heart of Los Angeles is witnessing a slow death of home sales. An increasingly widening financial chasm between renting and purchasing has transformed the American dream of homeownership into an elusive mirage for many. Local renters are discovering a staggering $1,853 monthly savings compared to homebuyers—a figure that places this coastal metropolis among the leaders in rental savings across the nation.

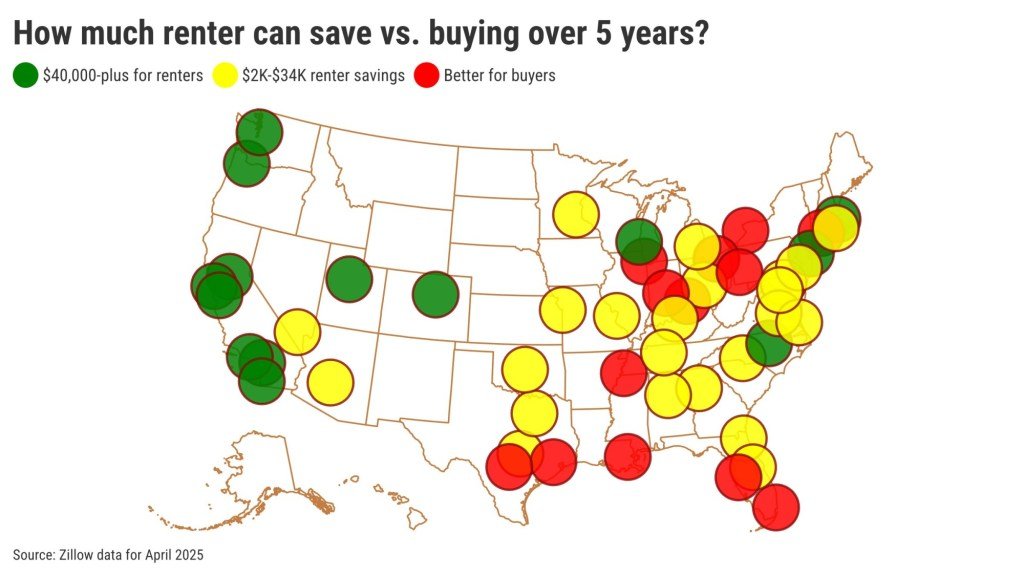

The Financial Landscape

According to a comprehensive study by Zillow, the stark reality of the rental market in Los Angeles and Orange counties is encapsulated by the high costs associated with renting individual homes, currently averaging a crippling $4,462 per month. This figure stands as the second-highest among the top 50 metropolitan areas, following only San Jose. For many, this seems like a bitter pill to swallow; however, purchasing a home in this market comes with an even heavier price tag. The median price of a home here is approximately $966,700, leading to monthly mortgage payments that hover around $6,315—a third-highest cost nationwide.

“The unavoidable reality is that the financial dynamics simply don’t add up for most people,” comments Dr. Linda Feldman, an economist with the Urban Housing Research Institute. “The savings from renting afford households greater security and flexibility without the weight of a significant down payment and maintenance fees.” Indeed, the calculated savings over five years can approach an eye-opening $105,000—an incentive that has led many to forgo the traditional path of homeownership.

Cost Analysis: The Numbers Speak

Breaking down the math reveals several critical insights into why individuals are choosing to rent rather than buy:

- Monthly Comparisons: Renters pay $4,462 while homeowners face $6,315.

- Five-Year Projection: Renting can save residents roughly $105,000 in total costs by accounting for inflation in average rent increases of about 3% per year.

- Down Payment Burden: For a typical buyer, the required 10% down payment represents $96,700—an sum that compounds the financial challenge.

The value of renting is underscored by its cushion against various costs that accompany home ownership. “Homeownership seems to be losing its luster, especially when you consider rising property taxes, insurance rates, and the often-overlooked homeowner association fees,” states Tom Wilson, a real estate analyst at Land & Associates. “Simply put, the appealing narrative of owning a home as an investment is being questioned by economic realities.”

Region Comparison: California’s Other Markets

The burden of homeownership is not unique to Los Angeles and Orange counties. Other Californian cities present strikingly similar results:

- San Jose: $350,000 savings from $4,508 rent versus $10,706 payments.

- San Francisco: $198,000 savings from $4,065 rent versus $7,564 payments.

- San Diego: $111,000 savings from $4,177 rent versus $6,133 payments.

- Sacramento: $58,000 savings from $2,800 rent versus $3,833 payments.

- Inland Empire: $43,000 savings from $3,085 rent versus $3,838 payments.

Across the rest of the United States, the narrative of renting versus owning varies dramatically. Nationwide, the average renter can anticipate only $5,000 in savings over five years. Notably, some metro areas like Indianapolis and San Antonio offer homebuyers financial advantages—an anomaly when compared to California’s ongoing housing crisis. “For those looking to purchase in Los Angeles, the costs—and challenges—additional to the base price are disheartening,” adds Dr. Feldman. “It’s not just about the house price; it’s the entire ecosystem of costs that come with it.”

Unpacking the Appeal of Renting

Beyond mere numbers, the psychological appeal of renting grows stronger in the face of such burdens. Renters enjoy a transient lifestyle, flexibility, and the ability to pivot their living situations as economic conditions evolve. In the taxing climate of rising prices, many professionals view renting as a practical alternative, offering peace of mind and financial agility. Sarah Lopez, a graphic designer in Los Angeles, embodies this sentiment: “I love my apartment. It isn’t perfect, but the thought of being locked into a mortgage while juggling rising living costs terrifies me.”

The paradox of wealth-building through homeownership might soon require reassessment. “Economic dynamics are shifting,” asserts Wilson. “The narrative surrounding homeownership is changing. It used to be that owning a house equated to financial literacy and success, but that narrative is under scrutiny.” As the conversation shifts from ownership to lifestyle and fluidity, Los Angeles may begin to reshape its housing narrative.

In a region where the cost of living continues to surge and the benefits of homeownership wane, the question remains: can traditional models of housing withstand the evolving nature of financial responsibility? For many Angelenos, the calculus is clear: renting is not just a stopgap; it’s a strategic choice in navigating both the onslaught of housing costs and the quest for solace in an ever-complicating market.